South Africa’s 2026 Budget consolidates a fiscal repair effort that has been building for several years. The deficit continues to narrow, the primary surplus strengthens, and debt stabilisation now anchors the forward outlook.

Markets have responded positively, with tighter bond spreads and last year’s S&P Global Ratings upgrade reinforcing improving sentiment. The question now is whether consistent delivery can turn that positive momentum into further upgrades, or whether implementation risks could blunt investor confidence.

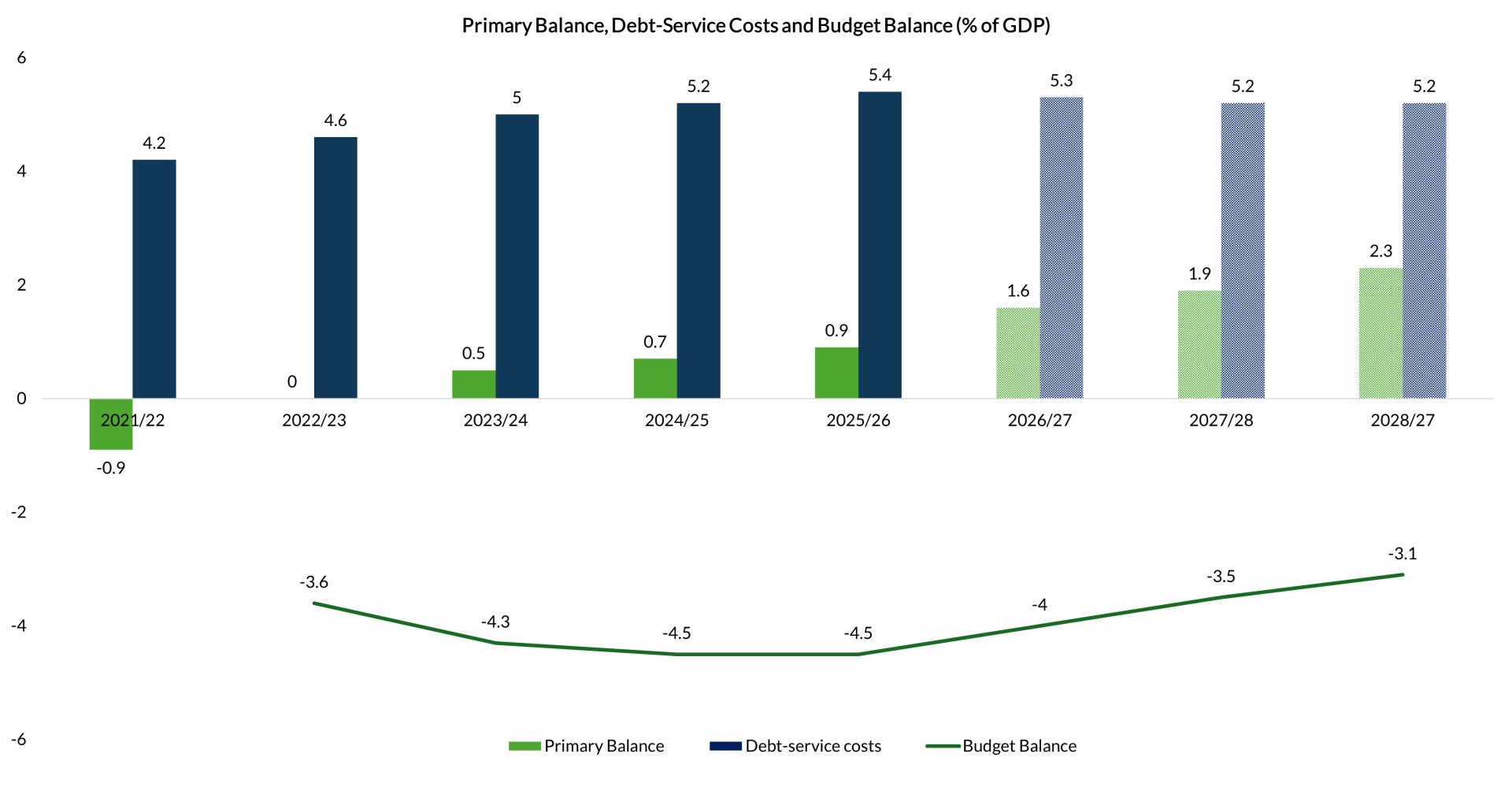

Fiscal Consolidation Supports Primary Surplus

The budget recorded a primary surplus of 0.9 per cent of GDP for 2025/26, and it is projected to expand to 2.3 per cent by 2028/29. That trajectory improves the balance before interest costs and creates the conditions for debt stabilisation. The credibility of the framework rests on maintaining expenditure discipline and continued structural reform over the medium term.

Source: National Treasury (Republic of South Africa) (n.d.) National Budget documents. Available at: https://www.treasury.gov.za/documents/National%20Budget/default.aspx

Stronger revenue supports this consolidation path. Gross tax revenue for 2025/26 rises by R21.3 billion, led by VAT and corporate collections. This has enabled government to withdraw R20 billion in planned tax increases and adjust income tax brackets for inflation, supporting households while maintaining fiscal discipline.

Spending pressures remain binding. Consolidated expenditure is projected to reach R2.58 trillion in 2025/26, with the social wage absorbing 60.2 per cent of non-interest spending.

Debt to GDP set to Peak as Interest Pressures Ease

For the first time in 17 years, South Africa’s debt trajectory has stabilised, with the debt-to-GDP ratio projected to peak rather than continue rising. The 2026 Budget Review estimates that gross debt will reach 78.9% of GDP in 2025/26, slightly above earlier projections due to weaker nominal growth and higher borrowing. Crucially, the ratio is expected to peak and then level off to 77.3% in 2026/27.

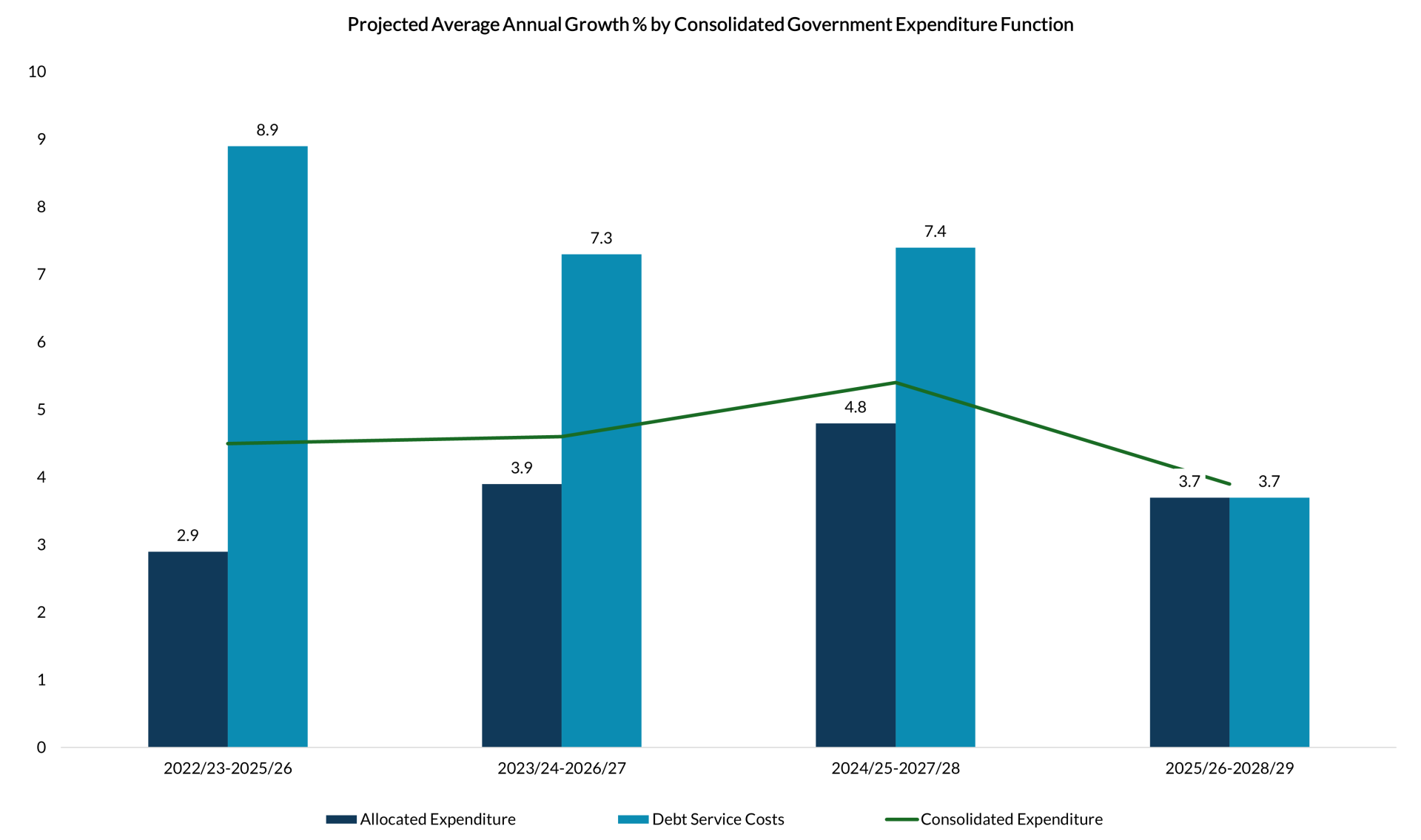

Debt-service costs are now projected to grow more slowly than total expenditure, easing pressure within the fiscal framework. In the 2022/23–2025/26 period, debt-service costs were projected to rise at 8.9 per cent per year, while allocated (non-interest) expenditure was expected to grow at 2.9 per cent. That gap resulted in real compression in frontline spending: schools, hospitals and infrastructure had to absorb restraint so that the state could meet its interest bill.

However, under the most recent projections, debt-service costs are expected to grow at 3.7 per cent in 2025/26–2028/29, down from 7.4 per cent in the previous projection window, and no longer materially faster than allocated expenditure, which declines from 4.8 per cent in 2024/25–2027/28 to 3.7 per cent in 2025/26–2028/29.

Source: National Treasury (Republic of South Africa) (n.d.) National Budget documents. Available at: https://www.treasury.gov.za/documents/National%20Budget/default.aspx

The shift appears structural rather than merely cyclical. Over the medium term, debt-service costs have been revised down by R10.6 billion, reflecting a sustained improvement in funding conditions, including lower market borrowing costs, a firmer rand and a marked decline in inflation. These improved fundamentals have fed directly into sovereign financing conditions. South Africa’s 10-year government bond yield has fallen to 7.89 per cent, its lowest level since March 2015, signalling strengthened and sustained investor confidence.

Private Sector Key to Infrastructure Investment Strategy

To deliver on economic growth targets, South Africa still requires substantial capital investment to address infrastructure gaps in energy, logistics and water. Delivering that investment within a stabilising debt framework is a delicate balancing act. In SONA 2026, the President committed R1 trillion to public infrastructure over the next 3 years. The Budget does not expand that headline pledge; it operationalises it within fiscal limits.

Rather than increase borrowing materially, Treasury reinforces a model that leverages private capital alongside public funds. In 2025, government issued its first sovereign infrastructure and development finance bond, raising R11.8 billion, signalling solid market appetite for financing public investment. Similarly, the Infrastructure Fund has been put forward as a blended finance mechanism designed to crowd in private capital. By using targeted public funding to de-risk projects and close viability gaps, it aims to make large infrastructure projects bankable. This matters because infrastructure at the required scale cannot be financed from the sovereign balance sheet alone.

Elections Put Budget Discipline Under Pressure

The social wage remains large in aggregate, but wage pressures and inflation constrain real per capita improvements in service delivery, particularly where municipal capacity is weak. Selective trimming of underperforming programmes support macro stability, yet they do little to shift structural unemployment or inequality. With municipal elections approaching, the strategy of doing more with less must translate into visible service gains or political support for consolidation will weaken.

Conclusion

South Africa’s fiscal outlook is no longer defined solely by containment. A credible primary surplus path, a stabilising debt ratio and easing debt-service pressure have shifted the debate from whether the numbers add up to whether the state can execute within them. That distinction matters: the framework creates room to protect priority spending and fund investment, but only if discipline is maintained and reforms translate into higher growth. Without growth, stabilisation remains fragile; with it, consolidation becomes self-reinforcing.

Government should lock in the gains by resisting new recurrent spending commitments, prioritising projects that can be delivered quickly and credibly, and removing the binding constraints in energy, logistics and water that hold back private investment. Fiscal repair has created a window of policy advantage. The next phase must be about implementation that raises potential growth — before political pressure and complacency close that window.

26 February 2026 Public Financial Management Transport Infrastructure Public Service Transformation Financing Growth & Development in Africa African Competitiveness

Jana De Kluiver

Political Economy Lead