For much of the past decade, South Africa has carried a higher sovereign risk premium. That premium has influenced more than bond markets. It has shaped the cost of financing transmission lines, logistics corridors, water systems, and large-scale infrastructure across the economy. When debt rises without a credible stabilisation path, capital responds. Yields rise, ratings weaken, compliance scrutiny intensifies, and that repricing becomes embedded in long-term borrowing structures and project finance models.

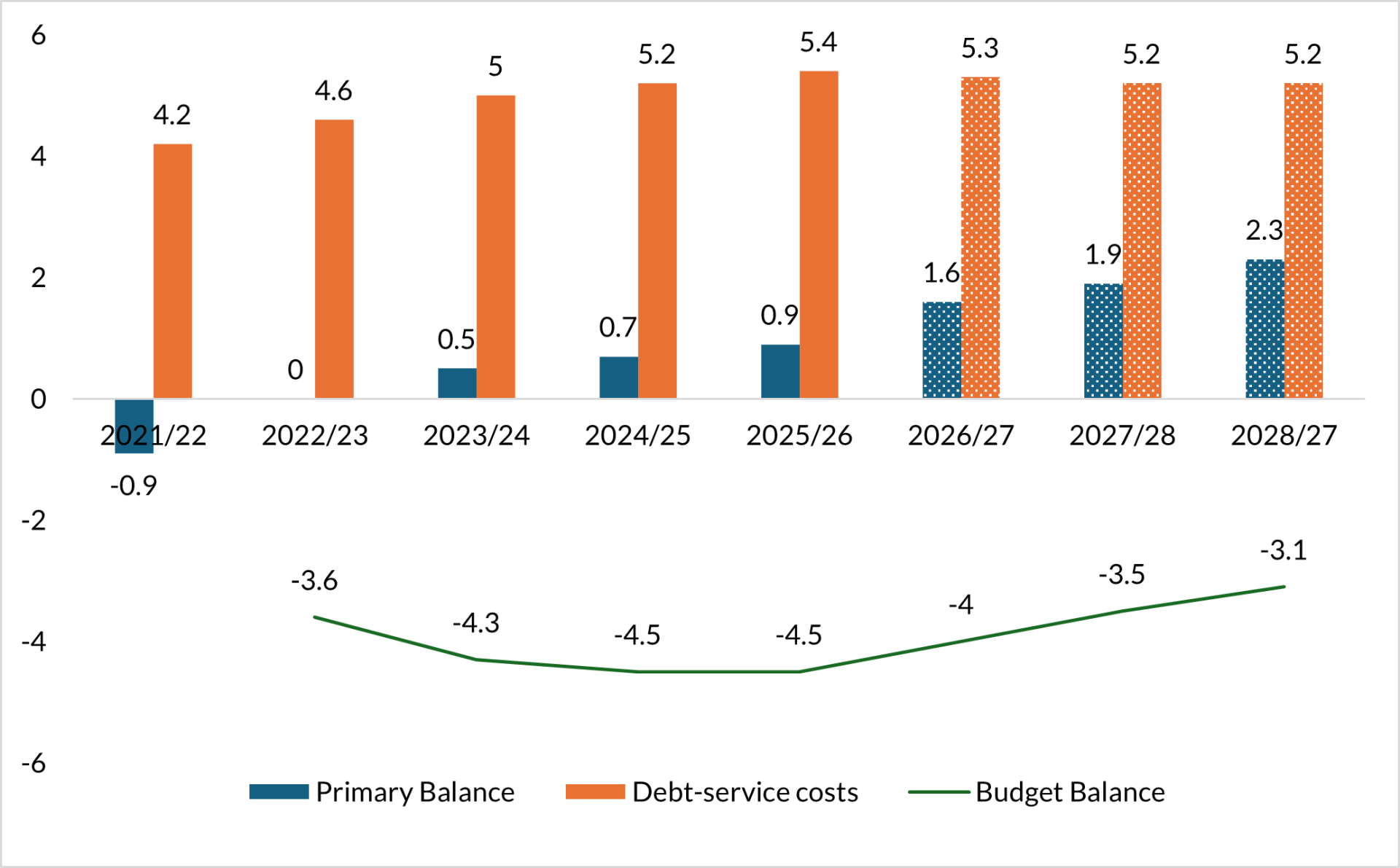

The 2026 fiscal trajectory signals a shift in direction. For the first time in over a decade, debt has stabilised Figure 1. This shift has not occurred in isolation. It reflects a series of structural adjustments centred on fiscal discipline, targeted capital allocation, and institutional reform.

South Africa has been removed from the FATF grey list, reducing compliance friction and improving its standing within global financial systems. S&P has revised its outlook from BB- to BB, signalling improving credit fundamentals and a more stable risk assessment environment.

At the same time, the emphasis within fiscal policy has begun to tilt toward strategic infrastructure investment and increased capital expenditure, rather than reliance on recurring consumption-based spending. This reallocation matters because capital expenditure expands productive capacity, while recurring expenditure maintains existing obligations. Over time, the balance between the two shapes both growth potential and debt sustainability.

Together, these developments point to reform that is structural and aimed at stabilising debt, improving the quality of public investment, and lowering the sovereign risk premium embedded in the cost of capital. However, these developments do not remove structural constraints, nor do they immediately transform fiscal fundamentals. What they do is influence how sovereign risk is assessed. And sovereign risk assessment feeds directly into infrastructure viability.

The Borrowing Cycle and Infrastructure Viability

Infrastructure financing depends on more than engineering capacity or procurement reform. It depends on the cost of capital available to the sovereign and to project sponsors. That cost is shaped by fiscal credibility, regulatory predictability, and institutional stability.

When sovereign risk increases, borrowing costs rise. Higher yields become embedded in public debt issuance and private financing structures. Investors demand compensation for volatility and policy uncertainty. Governments extend guarantees to crowd capital in, expanding fiscal exposure. As borrowing costs increase, project hurdle rates rise. Fewer projects meet financial viability thresholds. Reduced infrastructure delivery constrains productivity and growth, placing additional pressure on fiscal balances. Over time, the pricing adjustment reinforces itself.

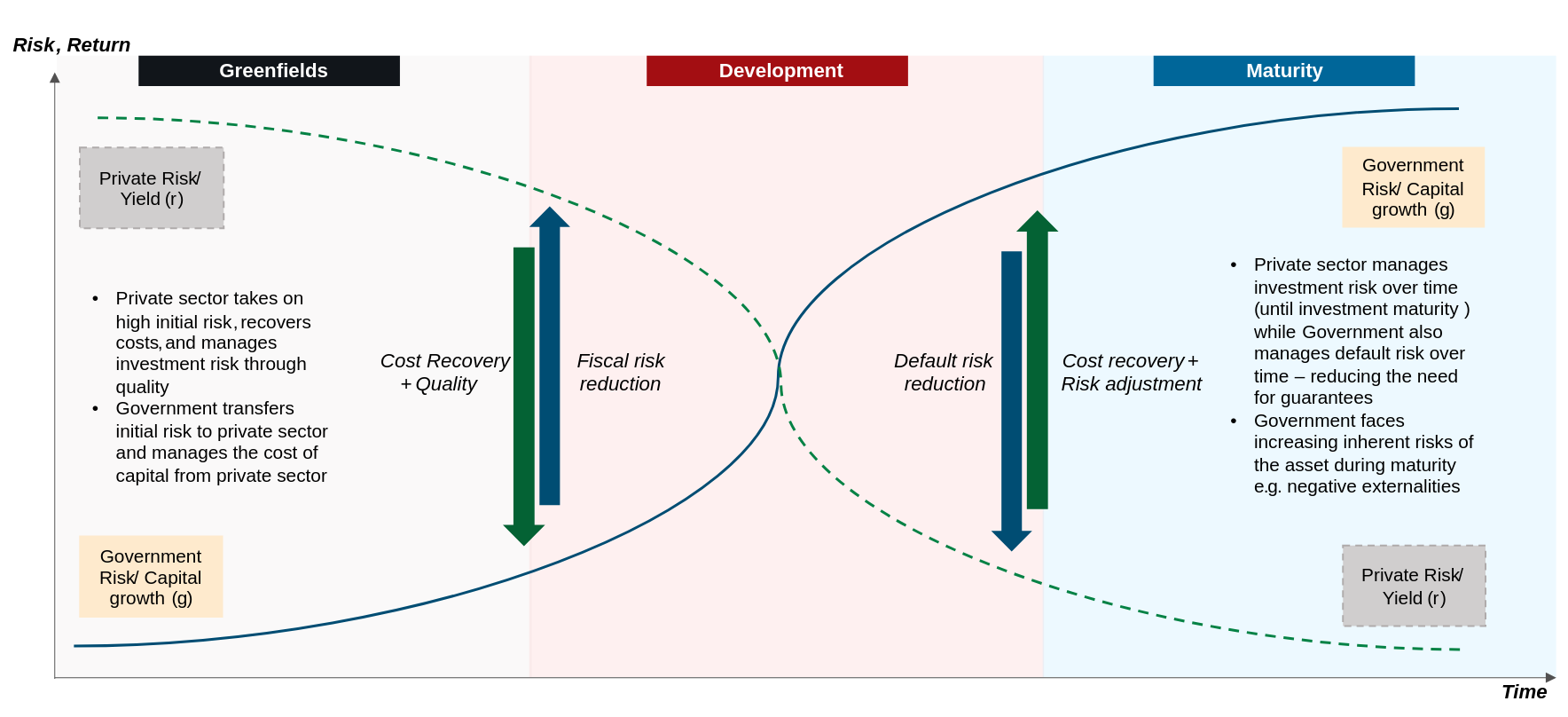

The risk-return interplay across infrastructure follows a recognisable lifecycle Figure 2. In early-stage or greenfield environments, private capital demands elevated yields because uncertainty is highest. Construction risk, policy volatility, and revenue unpredictability are priced aggressively. At this stage, governments often absorb part of the exposure through guarantees or balance sheet support, effectively transferring initial risk to the public sector to attract private participation. The cost of capital reflects that uncertainty.

As projects move into development and operational phases, risk redistributes. Construction exposure declines, cash flow visibility improves, and default risk becomes more measurable. Yield expectations moderate accordingly. Financing structures shift from absorbing risk to managing and adjusting it. Pricing changes because uncertainty reduces.

By the time assets reach maturity, private risk yields are materially lower. Capital growth becomes more stable, and participation shifts toward long-duration investors who prioritise predictability. At this stage, financing is less about compensating for volatility and more about allocating capital efficiently across productive assets.

Sovereign positioning influences this entire curve. When fiscal credibility weakens and spreads widen, the full risk-return structure shifts upward. Greenfield projects become expensive, development phases lengthen, and guarantees expand. Conversely, when fiscal discipline strengthens and spreads compress, the curve shifts downward. Early-stage capital becomes less punitive. Development-stage financing stabilises. Mature assets attract long-term capital without excessive risk pricing.

Structural reform influences this pricing mechanism. Fiscal consolidation, governance improvements, and regulatory discipline reduce uncertainty. As uncertainty declines, sovereign risk margins narrow. As margins narrow, financing costs fall. When financing costs fall, infrastructure that was previously marginal becomes viable. Over time, this expands the space for sustained investment rather than episodic funding.

Repricing Through Market Integration: The Zambia Case

Zambia provides a complementary illustration of how structural reform intersects with pricing. Following its debt restructuring process, Zambia has called for its domestic debt market to be included in major global bond indices. The objective is practical. Inclusion in benchmark indices increases transparency, standardisation, and liquidity. It broadens the investor base and integrates domestic instruments into global pricing frameworks.

When domestic debt is incorporated into widely tracked indices, it becomes part of comparative valuation models used by global investors. Risk is assessed relative to peers rather than treated as isolated exposure. Capital flows deepen. Liquidity improves. Volatility moderates. Pricing becomes more efficient because it reflects broader participation and clearer benchmarks.

For infrastructure financing, these dynamics matter. Efficient pricing reduces distortions in borrowing costs. Broader participation lowers concentration risk. Deeper liquidity strengthens domestic capital markets and reduces reliance on short-term funding structures. Over time, these shifts expand the ability of domestic systems to support long-duration infrastructure investment.

Zambia’s approach highlights a broader principle: structural reform is not limited to fiscal containment. It includes improving market architecture so that risk can be evaluated, compared, and priced with greater accuracy. Fiscal stabilisation and market integration operate together to influence how capital behaves.

Sovereign Wealth Funds and Long-Duration Capital

These pricing dynamics are central to the ongoing conversation about mobilising sovereign wealth funds for Africa’s infrastructure transformation. Sovereign wealth funds allocate capital over long horizons and across diversified portfolios. Their decisions are based on risk-adjusted return supported by institutional predictability and pricing stability.

For several years, many African markets have been priced at the upper end of acceptable risk thresholds. The opportunity has been visible, but the cost of uncertainty has been embedded in required returns. Elevated spreads, volatility, and governance concerns have shaped participation decisions.

Structural reform alters that calculation incrementally. Debt stabilisation narrows spreads. Removal from grey listing reduces compliance friction. Ratings outlook improvements signal improving fundamentals. Market integration initiatives enhance liquidity and comparability. As these elements accumulate, pricing stabilises and long-duration capital becomes more viable without excessive guarantees or fiscal distortion.

Mobilising sovereign wealth capital therefore depends not only on project structuring or blended finance innovation, but on sustained reform that lowers the sovereign risk premium over time. When risk is priced more efficiently, infrastructure becomes investable on its own merits rather than through extraordinary support mechanisms.

Direction, Discipline, and the Cost of Capital

Capital markets respond to trajectory. Sustained fiscal discipline narrows risk premiums over time, while inconsistency widens them. Infrastructure transformation depends on maintaining a trajectory that reduces uncertainty and lowers the cost of capital durably.

Lower sovereign risk reduces borrowing costs. Lower borrowing costs expand the number of projects that can meet financial thresholds. Greater infrastructure delivery strengthens productivity and growth. Stronger growth reinforces fiscal resilience and supports further risk compression. Over years, relatively small adjustments in spreads translate into material differences in long-term capital allocation.

Infrastructure debates often centre on funding gaps and pipeline announcements. Beneath those discussions sits a more fundamental variable: how risk is priced and how efficiently markets absorb it. Structural reform influences that efficiency. Efficiency in pricing determines whether plans convert into financed projects or remain conceptual.

The significance of reform lies in its cumulative effect on cost. When credibility improves, risk is priced lower and infrastructure becomes more financeable. When credibility weakens, pricing adjusts upward and viability narrows. Over time, those pricing shifts shape development outcomes in ways that are rarely visible in a single fiscal year but decisive over decades.

Reform Determines Viability

Infrastructure does not stall because ambition is absent. It stalls when the cost of capital remains elevated and risk is priced inefficiently.

Fiscal stabilisation, market integration, and institutional discipline influence that pricing over time. When risk premiums compress sustainably, borrowing costs decline. When borrowing costs decline, more projects meet viability thresholds. As viability expands, infrastructure moves from concept to execution.

The adjustment is gradual, but its implications are structural.

Reform does not guarantee transformation. It alters the conditions under which transformation becomes possible.

And in infrastructure finance, those conditions determine whether long-term capital participates at scale, or remains cautious, expensive, and selective.

Ready to move from intention to implementation? Get in touch at

27 February 2026 Minerals & Mining Energy Efficiency & Conservation Policy & Regulatory Affairs African Competitiveness Energy Transition