Africa has expanded accounts, mobile money and digital payments at scale. But too few households and small firms can convert that access into savings, resilience, enterprise and capital growth. The next phase of inclusion is not about more accounts alone; it is about deeper economic participation. This study demonstrates some of the key considerations to unlock true deeper economic participation, and the need for interventions that respond to the real needs and dislocations of each market, based on their bespoke maturity and nuances.

Access has advanced, but participation remains thin

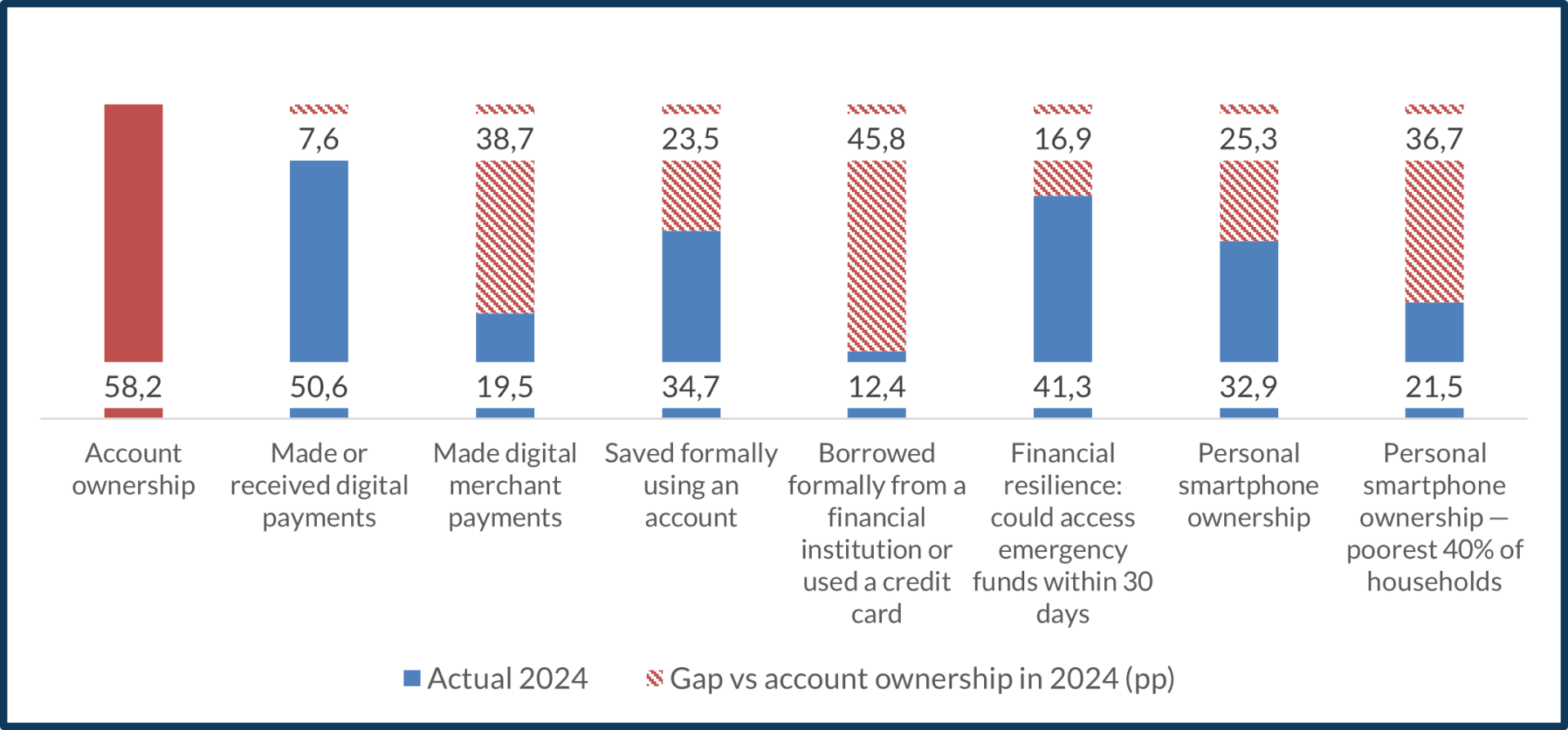

58.2% SSA adults with an account in 2024 | 19.5% SSA adults making digital merchant payments in 2024 | 12.4% SSA adults borrowing formally in the past year |

32.9% SSA adults owning a personal smartphone; 21.5% among the poorest 40% | 98% South Africa formal financial inclusion rate in 2023 | US$402.2bn Africa’s annual financing gap to accelerate structural transformation by 2030 |

Figure 2: SSA Snap Shot (African Development Bank Group. 2024. Scaling up financing is key to accelerating Africa’s structural transformation; FinMark Trust. 2024. FinScope Consumer 2023, South Africa – Media Release; World Bank. 2025. Little Data Book on Financial Inclusion 2025)

For much of the past decade, financial inclusion in Africa has been measured by a simple question: how many adults have an account? That metric still matters, but it is no longer enough. The more strategic question is whether finance allows households and small businesses to participate more fully in the economy - by making and accepting payments, building savings buffers, managing risk, accessing working capital, and investing in productive opportunity. If inclusion stops at account opening, Africa gets more wallets, but not more balance sheets.

Our core thesis is that Africa’s next inclusion leap is not opening more accounts. It is converting everyday cashflows into usable liquidity, credible data, risk protection and investable savings - so that more people can participate in the economy through the financial system, not merely touch it.

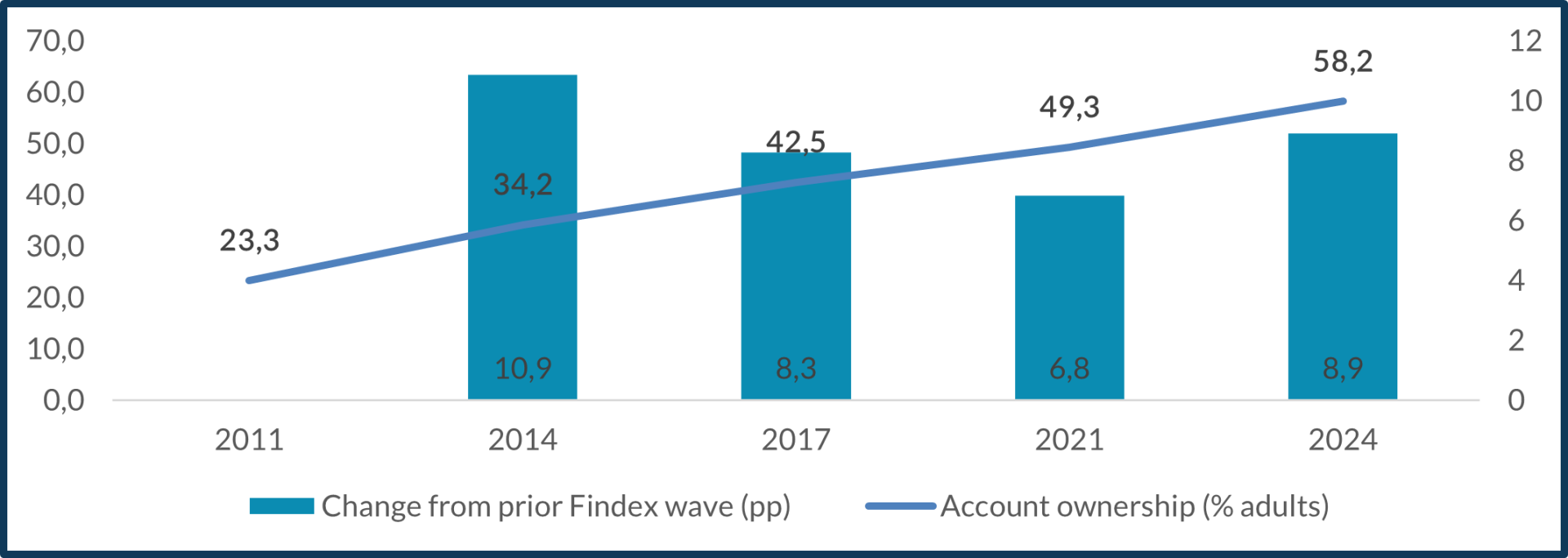

Across Sub-Saharan Africa, 58.2% of adults had an account in 2024 and 50.6% made or received a digital payment in the previous year. Yet only 19.5% made a digital merchant payment, only 12.4% borrowed formally, and smartphone ownership was just 32.9% overall and 21.5% among the poorest 40% of households. In 2024, Sub-Saharan Africa accounted for over 1.1 billion registered mobile money accounts and around US$1.1 trillion in transaction value, underlining the scale of digital financial infrastructure already in place across the region, according to the GSMA State of the Industry Report on Mobile Money 2025 and the World Bank Little Data Book on Financial Inclusion 2025. The implication is clear. Africa’s constraint is no longer simply the absence of rails; it is the shallow conversion of access into everyday participation, resilience and capital formation.

South Africa makes the point even more sharply. Formal financial inclusion is already 98%, yet inclusion is often passive rather than productive. FinScope Consumer South Africa 2023 shows that 10.4 million South Africans, equivalent to 76 percent of the measured group, withdraw all money from their bank account after receipt. This points to a system with high formal inclusion, but shallow digital retention and weak day-to-day participation. The same study shows that digital merchant payment usage is only 37% among rural poor consumers and 40% among urbanised workers, compared with 88% among wealthy city segments. In other words, being banked does not automatically mean being able to live, save or trade digitally on viable terms.

An access-first narrative can therefore overstate progress. It treats an opened account as a completed outcome, when in reality it is only the start of a chain: identification, onboarding, receipt of funds, retention of value, merchant acceptance, data creation, creditworthiness, savings accumulation, risk protection and eventually investment. Break any link and the system collapses back to cash.

Financial inclusion is now a systems problem

The new frontier is to turn cashflows into economic participation. That requires multiple parts of the ecosystem to align at the same time. AIA’s view is that six threads matter most.

1. Formal Identity and onboarding. Without reliable identity and proportionate know-your-customer rules, accounts remain hard to open or too constrained to use. In the 36 Sub-Saharan African economies where the World Bank collected data, 78% of eligible people above age 15 had a formal ID, but the gaps remain large and concentrated among poorer, rural and marginalised groups. High-coverage countries can scale onboarding faster; low-coverage countries cannot, as highlighted in the World Bank Trends in Access to ID in Sub-Saharan Africa and the World Bank Access to ID in SSA Report.

2. Useful payment rails and last-mile acceptance. Digital money only works if it can circulate. If wages, grants or remittances arrive digitally but groceries, transport, utilities and micro-merchants still require cash, consumers will cash out immediately. This is why low-value instant payments and merchant acceptance matter more than account opening alone. South Africa’s payments modernisation agenda, including the launch of PayShap, is intended to deepen digital financial inclusion by making low-value digital payments more convenient and by reducing reliance on cash for consumers and small businesses, as outlined in the SARB PayShap launch press release and the South African Reserve Bank Digital Payments Roadmap Report.

3. Digitised high-volume cashflows. The fastest way to deepen inclusion is to digitise the payment streams that recur at scale - government transfers, wages, remittances, and agricultural value-chain payments. World Bank data show that more than 140 million adults in Sub-Saharan Africa still receive agricultural sale payments in cash, including 66 million women. Digitalising these flows creates a practical on-ramp into savings, insurance and input finance rather than a standalone wallet with no onward use, as explored in the World Bank Digitalising Agricultural Payments in Sub-Saharan Africa and the World Bank Agricultural Payments Report

4. Data-to-risk infrastructure. Inclusive finance becomes economically powerful when transaction histories can support risk assessment, savings behaviour, insurance take-up and working-capital finance. Yet the latest IFC-World Bank estimate puts the Medium-to-Small Enterprises (MSME) finance gap across 119 emerging markets and developing economies at about US$5.7 trillion, with 40% of formal MSMEs credit-constrained. Thin usage produces thin data; thin data keeps pricing conservative or punitive; and punitive pricing suppresses productive borrowing in the very segments that need it most, as outlined in the World Bank SME Finance overview.

5. Trust, recourse and consumer capability. People do not keep value in the system if disputes are slow, fraud losses are final, or product terms are opaque. This is especially important for first-time and low-confidence users. Financial literacy matters, but so does visible recourse - clear liability rules, rapid resolution and product design that matches irregular incomes. Without that, usage stagnates even where infrastructure exists.

6. The asset layer: savings, insurance and investment. Payment access is useful, but development impact comes when households can build buffers, insure against shocks, and allocate capital to productive uses. This matters because financial inclusion is not only a social imperative, but a market-development lever. The African Development Bank estimates that the continent needs to close an annual financing gap of US$402.2 billion by 2030 to accelerate structural transformation, as highlighted in the African Development Bank African Economic Outlook 2024 and the African Development Bank report on scaling up financing for Africa’s structural transformation. At the same time, the International Labour Organisation estimates that 83.1% of employment in Africa is informal, rising to 86.3% in Sub-Saharan Africa, according to the International Labour Organisation Africa Informality Statistics. In practical terms, that means a large share of households and enterprises still operate with limited access to formal savings, risk protection, and productive finance.

Cross-border household cashflows illustrate the same leakage. Sub-Saharan Africa remains the most expensive region in the world to send remittances to, with an average cost of 8.78% in Q1 2025, according to the World Bank Remittance Prices Worldwide database. For many families, that fee is money lost before it can become school-fee savings, business inventory, agricultural inputs or home improvement.

Why this matters for enterprise growth

This is where the financial inclusion conversation must change. If a market focuses only on consumer onboarding, it creates transaction endpoints. If it focuses on participation, it builds a pipeline from cashflow to capability: payment history to credit assessment, savings to resilience, insurance to shock absorption, and domestic pools of capital to enterprise finance.

The development upside is large. Even South Africa - where inclusion rates are high - shows how quickly the system hollows out when resilience is weak: 40% borrowing to buy food is not evidence of healthy financial deepening; it is evidence that formal access and financial stress can coexist, as highlighted in the FinScope Consumer South Africa 2023.

This matters for industrialisation, agriculture, housing and jobs. Small firms cannot scale on thin, volatile cashflows alone. They need savings buffers, working capital, payment histories, insurance protection and affordable risk pricing. Households need the same tools for consumption smoothing and investment in education, transport and shelter. In that sense, financial inclusion should not sit at the edge of social policy. It should be treated as part of SME policy, agricultural modernisation, domestic savings mobilisation and market development.

South Africa is both a warning and an opportunity

South Africa is often presented as a success story because account access is high, which is true. But it is also a warning against confusing access with participation. The FinScope evidence suggests that the real bottlenecks now lie in low-value payment economics, township and rural merchant acceptance, dispute resolution, irregular-income savings design, and responsible credit pathways. These are not “nice to have” improvements at the edge of the system; they are the mechanisms that determine whether digitally received money stays digital long enough to become useful, as highlighted in the FinScope Consumer South Africa 2023.

98% Adults “formally” financially included | 76% Adults always withdraw all cash from their bank account | 40% Adults borrow money to buy food |

That is why South Africa deserves attention far beyond its own borders. It is showing the rest of the continent what the next generation of inclusion challenges looks like once basic access has largely been solved. The lesson is simple: a banked population can still be economically excluded from everyday digital commerce if costs are wrong, trust is weak, or relevant use cases are absent.

Market development through Financial Inclusion

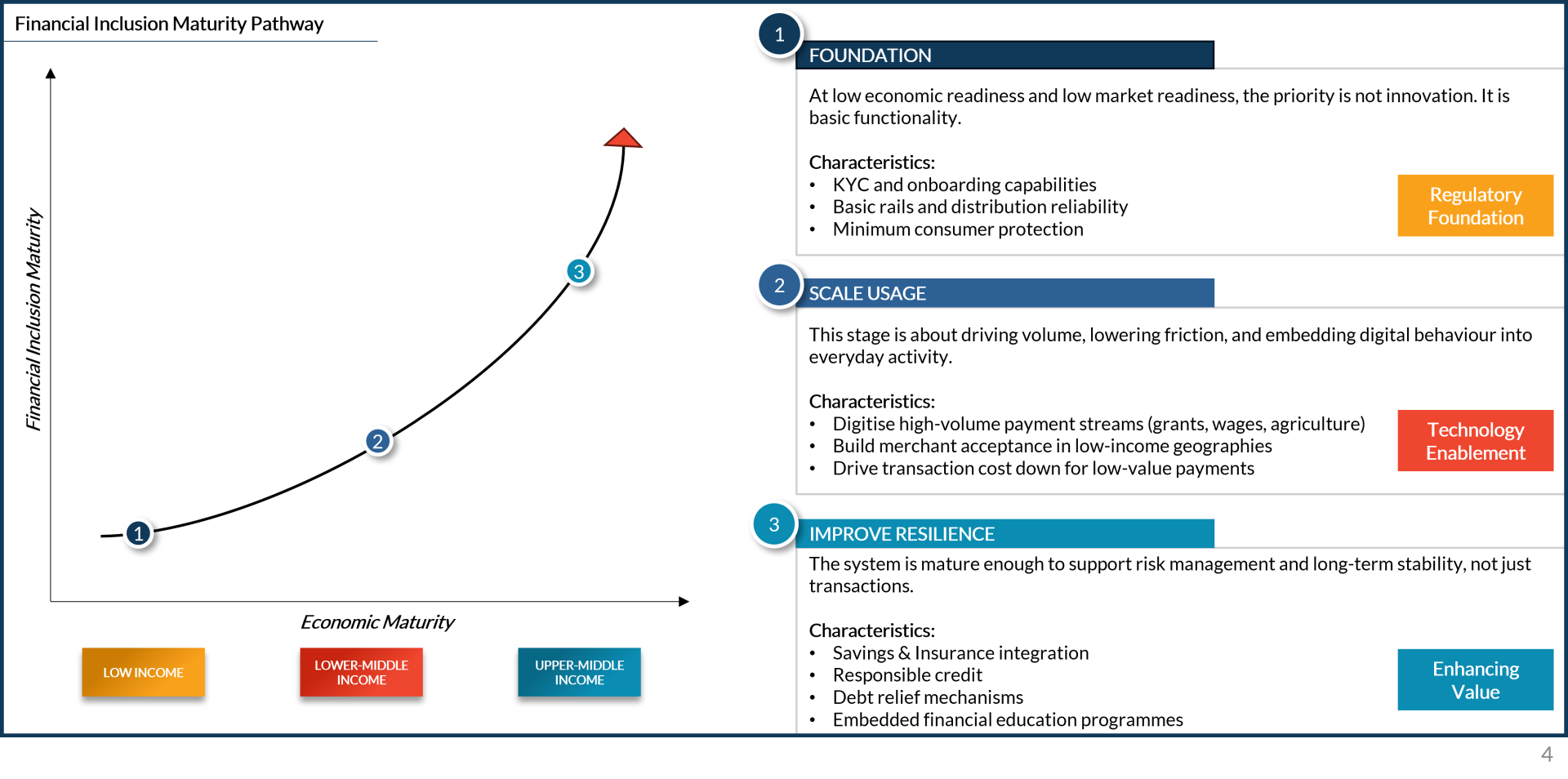

Financial inclusion should not be treated as a binary outcome measured by account ownership alone. In lower-maturity markets, the priority is to establish basic access and trust in the system. In more developed markets, the requirement shifts toward deepening usage, improving resilience, and enabling productive participation in the economy. The appropriate lens, therefore, is not simply whether people are included, but what the financial system enables them to do at each stage of market development.

The framework below sets out a phased maturation pathway for financial inclusion, aligned to the structural maturity of the economy. It recognises that inclusion deepens through three sequential but overlapping stages: Foundation, Scaled Usage, and Improve Resilience. These stages are not arbitrary. They reflect the economic logic that financial systems tend to evolve from basic transactional capability, toward embedded usage at scale, and ultimately toward wealth preservation, risk management, and productive capital formation [1, 4, 5, 7, 8, 11, 13, 16].

As economies move from low income to lower-middle-income and then upper-middle-income status, the strategic emphasis must also shift.

- In low-income markets, inclusion is primarily about establishing a foundation: identity, account access, payments capability, agent distribution, and a minimum level of regulatory confidence.

- In lower-middle income markets, the key challenge becomes scaled usage: moving beyond dormant accounts toward frequent, trusted, low-friction usage across wages, remittances, merchant payments, agriculture, and small enterprise activity.

- In upper-middle-income markets, the system must improve resilience: enabling savings, insurance, formal credit, long-term investment participation, and broader financial behaviours that support household stability and enterprise growth.

The core point is that financial inclusion must mature in line with market readiness. Pushing sophisticated products into an economy that lacks basic trust, infrastructure, or regulatory capability is inefficient. Equally, stopping at access in a more mature economy leaves value on the table and traps consumers in shallow participation.

Financial inclusion in Africa now needs to move from access to agency, from wallets to balance sheets, and from payment rails to capital formation. The continent already has proof that distribution can scale. The next test is whether that distribution can help households absorb shocks, help informal traders and MSMEs grow, and help domestic savings finance Africa’s own structural transformation.

The question is no longer whether Africans can be brought into the financial system. It is whether the financial system can be redesigned so that more Africans can participate fully in the economy through it. The future of inclusion will belong to the institutions that understand that difference early - and act on it.

Speak to our team about how financial inclusion can unlock market growth and long-term value lwandle.f@africaia.com.

20 March 2026 Retail & Commercial Banking Insurance & Risk Management Asset & Wealth Management Digital Transformation Financing Growth & Development in Africa