Moody’s has shifted the country’s sovereign credit outlook from stable to positive, while keeping the rating unchanged at Ba2. The agency cited an improvement in fiscal metrics, the accumulation of larger primary surpluses, and sustained commitment to structural reforms, with implementation outcomes becoming increasingly evident. Similarly, S&P upgraded South Africa’s rating in 2025.

However, bond investors moved even earlier. South Africa's sovereign bond market has already priced in a meaningful improvement in the country's credit story — one driven by a combination of monetary discipline, fiscal consolidation, and a more stable political environment than many investors had anticipated.

Three Shocks, a Changing Story

In the past six years, the world economy has faced numerous shocks. What is noticeable throughout this period is how these shocks have affected South Africa’s government 10-year bonds.

When the COVID-19 pandemic hit in early 2020, investors rushed into developed-market safe havens. As a result, developed-market yields such as US and UK yields fell sharply. South Africa was absorbing the shock with a fragile economy, sustained underinvestment in critical infrastructure, and an institutional credibility gap accumulated over nearly a decade of state capture, among other constraints. As a result, South African yields increased sharply.

The Russia–Ukraine war resulted in another shock in 2022. However, the relative impact on local bonds was less severe than during the COVID-19 pandemic. As a result, South Africa’s underperformance relative to developed markets narrowed.

The current crisis in the Middle East, which has led to the closure of the Strait of Hormuz, culminated in another shock. While global bond markets have again come under pressure, the reaction in South African bonds has been markedly more muted than in many developed markets. In effect, South Africa’s relative resilience across these three episodes appears to have improved, though three observations are insufficient to confirm a structural shift.

The compression in South Africa’s 10-year bond yield and narrowing spreads versus US and UK benchmarks signal a lower sovereign risk premium applied to South Africa by investors, improving government funding conditions and strengthening the investment case for South African assets. South African government rand-denominated bond yields have fallen by roughly 310 basis points over the past two years, with the 10-year yield now trading around 8.9%, down from a peak of approximately 12% in mid-2024. Over the same time period, the spread between South African and US 10-year yields has narrowed from around 770 basis points in mid-2024 to roughly 430 basis points today. Similarly, the gap with UK gilts has narrowed from 800 to just under 400 basis points.

Why South Africa’s Bond Yields Have Held Up

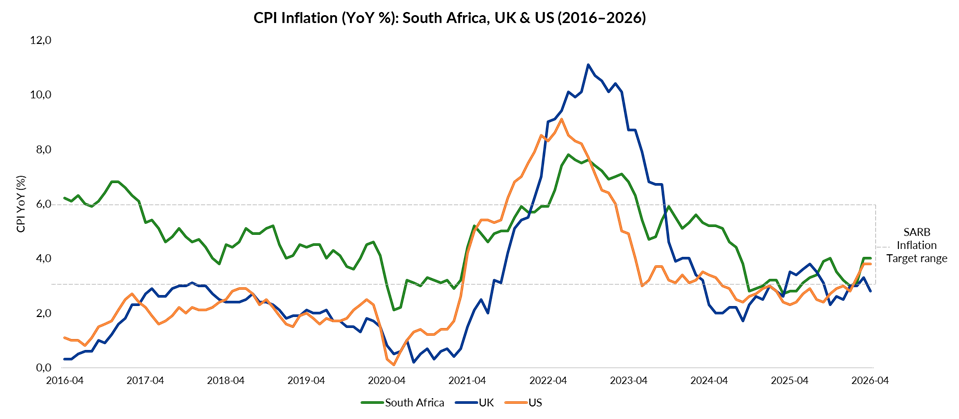

The South African Reserve Bank (SARB) has done something few of its peers managed: it has pushed for a lower inflation target, and then demonstrated the competence to meet it. Through early 2026, headline inflation had been tracking close to 3%, though a subsequent surge in fuel prices pushed the April reading to 4.0% and prompted the SARB to raise the repo rate by 25 basis points to 7% in May 2026 — its first hike since 2023.

Entities such as the Bank of England and the US Federal Reserve, both of which were slower to react to the price surge that began in early 2021, allowing inflation to become entrenched, then faced painful tightening cycles to regain lost ground. South Africa's

Similarly, the government has made progress on structural reforms. The reform agenda has encompassed electricity supply, logistics and freight infrastructure, immigration policy, and the partial unbundling of state-owned enterprises. Most notably, load-shedding, which strangled output and deterred investment for nearly a decade, has not occurred for over a year. Progress on logistics, ports and immigration policy has been slower, but the direction of travel remains constructive.

A perceived increase in political stability has reinforced this trend. The Government of National Unity (GNU), the ten-party coalition formed after the ANC lost its outright majority in 2024, has delivered more continuity than markets expected. Investors had priced in policy disruption, which did not materialise. The GNU has not produced a reform boom, but it has kept policy on a predictable path and reassured investors that institutional checks on policy remain functional. That stability has rested on a narrow factional equilibrium rather than a durable institutional consensus — which is why it also features in the risk section.

What Could Reverse the Rally

The bond market has priced improved inflation outcomes and lower political risk. Those two assumptions now face tests simultaneously.

The consumer price index (CPI) increased to 4.0% in April 2026 from 3.1% in March 2026, driven mainly by sharp fuel price increases. This is the highest inflation print since August 2024, when the headline rate was 4.4%, driven mainly by higher fuel prices. If oil prices remain elevated, the SARB may need to pause or tighten policy.

Seasonal weather conditions introduce an additional supply-side variable. National Oceanic and Atmospheric Administration Climate Prediction Centre currently assigns an 82% probability of El Niño developing during May–July 2026 and a 96% probability of El Niño persisting into December 2026–February 2027. This period follows the start of South Africa’s summer crop planting season in October. Elevated oil prices are simultaneously driving up fertiliser input costs.

A drought scenario would put upward pressure on the food CPI at a time when energy-driven inflation is already pushing up inflation. Current grain reserves, supported by two consecutive strong harvests, provide a near-term buffer but do not insulate the inflation outlook from a sustained dry spell. The combined effect would narrow the SARB's policy space and put pressure on the inflation assumptions currently priced into the bond market.

Political stability presents another risk. Local government elections are set for 4 November 2026, and the coalition parties in the GNU must now campaign against each other at the municipal level, potentially increasing friction. Similarly, the Constitutional Court’s Phala Phala ruling has revived impeachment proceedings against President Ramaphosa and could accelerate succession battles inside the ANC. Historical ANC succession contests have at times destabilised coalition arrangements, which is why this may be regarded as a tail risk rather than a base case.

The Window Now Open

Global macro-conditions, political and economic, are arguably the most difficult and complex they have been in a long time. What the bond market is quietly signalling is that South Africa has navigated this turbulence better than its starting point suggested it would. That is a meaningful shift, even if it remains incomplete.

The opportunity for South Africa now is to build on the solid progress made by maintaining the established monetary and fiscal anchors and harnessing the lower cost of capital that this would bring. This would not only empower South Africa to sail the global ‘sea of storms’, but to fundamentally alter the trajectory of its economy over the coming decades.

29 May 2026 Financing Growth & Development in Africa

Jana De Kluiver

Political Economy Lead