The Structural Decline in Domestic Refining

For decades, South Africa’s liquid fuels system was built around refining capacity. Crude oil was imported, processed domestically, and distributed inland. Refining acted as both production engine and buffer. It absorbed volatility in global crude markets and provided operational flexibility when shipping schedules shifted.

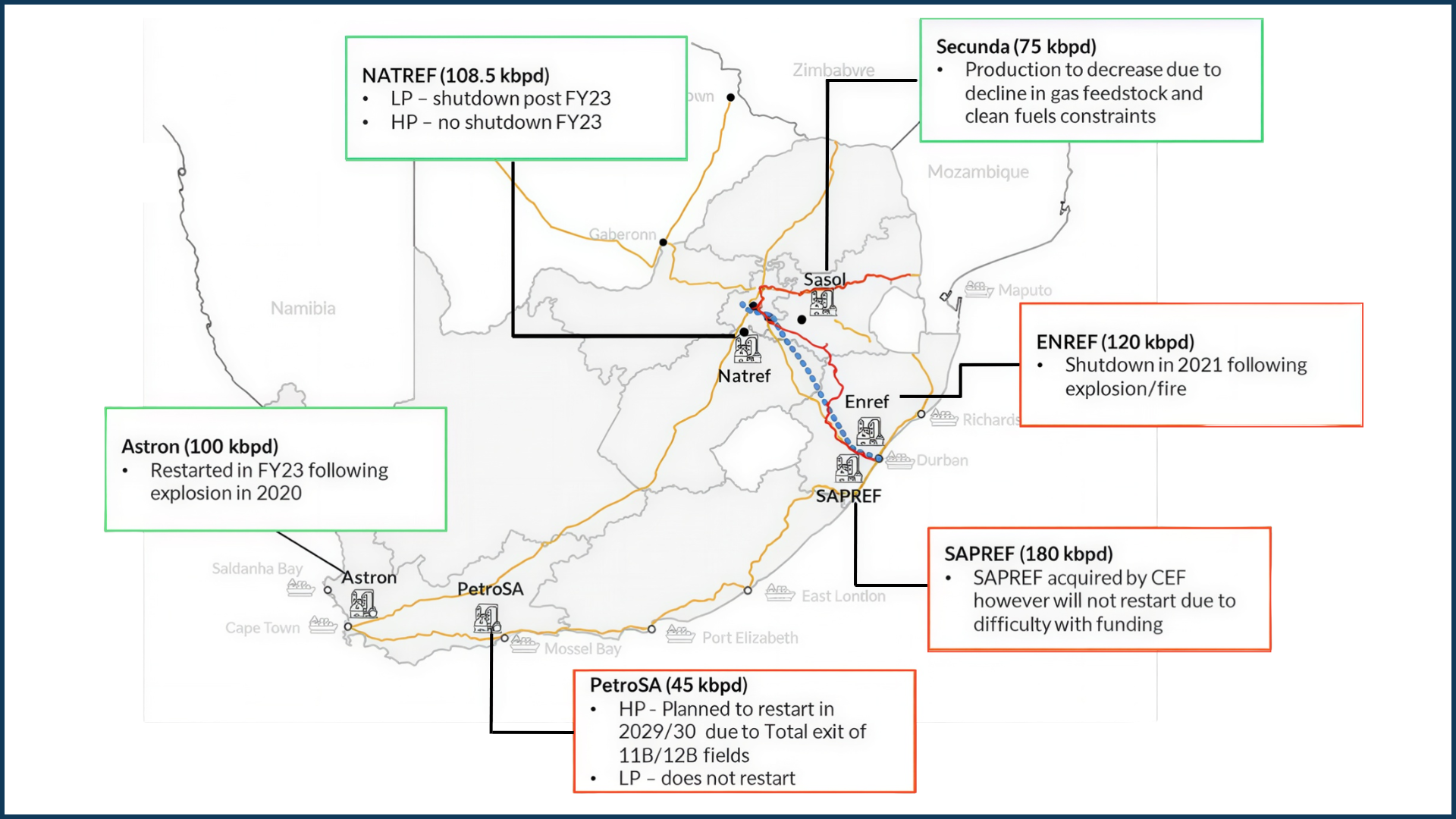

Effective national refining capacity has declined significantly from historic levels of roughly ~628,000 barrels per day as shown in Figure 1. Sapref remains offline. Enref has exited refining. PetroSA ceased operations due to feedstock constraints. Natref has reduced throughput while Secunda remains operational.

As refining capacity has withdrawn, imports of refined product have increased to fill the gap. Diesel, petrol and jet fuel now enter the country in larger volumes already processed. The value chain has shifted downstream.

The Import Transition and Its Implications

In a refinery-based system, crude imports are planned around refinery configuration and feedstock requirements. Refineries cannot run any crude indiscriminately. They depend on compatible crude slates, operating conditions and processing economics. Even so, domestic refining provides an additional buffer between import arrivals and final product availability, because crude can be converted locally into multiple products rather than relying entirely on imported refined cargoes.

In an import-based system, refined product arrives in discrete cargoes. Supply cadence therefore depends more directly on freight markets, global refinery output, port throughput and geopolitical stability.

South Africa now depends more directly on global product markets, shipping corridors and freight availability. Delays in vessel arrivals, congestion at ports, and volatility in international product spreads affect domestic availability more immediately than before.

As import dependency rises, the system becomes more sensitive to logistics constraints. The buffer once provided by refining must now be provided by storage and inventory cover.

The question is no longer how much crude can be processed domestically. It is how much refined product can be absorbed, stored, and redistributed without disruption.

Strategic Stockholding and the IEA Benchmark

In an import-dependent system, stockholding is not a regulatory metric but a resilience buffer. The IEA’s 90-day benchmark exists precisely because import economies are exposed to external shocks they cannot control. These stocks are strategic reserves, distinct from commercial inventories. They are designed to provide supply continuity during major global disruptions.

South Africa is not an IEA member and does not operate under a binding 90-day net import requirement. Historically, the country relied on a combination of strategic crude holdings and commercial inventory buffers supported by domestic refining capacity.

In an import-led system, refined product, not crude, becomes the critical vulnerability. Strategic crude reserves provide limited protection if domestic refining capacity is constrained. The resilience metric shifts from crude stockpiles to refined product availability and storage sufficiency.

IEA countries design storage capacity around quantified days-of-cover targets. In South Africa, days-of-cover are influenced by commercial inventory levels, port throughput rates, and storage constraints. In a stable global environment, this may function adequately. In a disrupted environment, the margin can narrow very quickly.

Port Concentration, Import Flow Dynamics and Demand Concentration

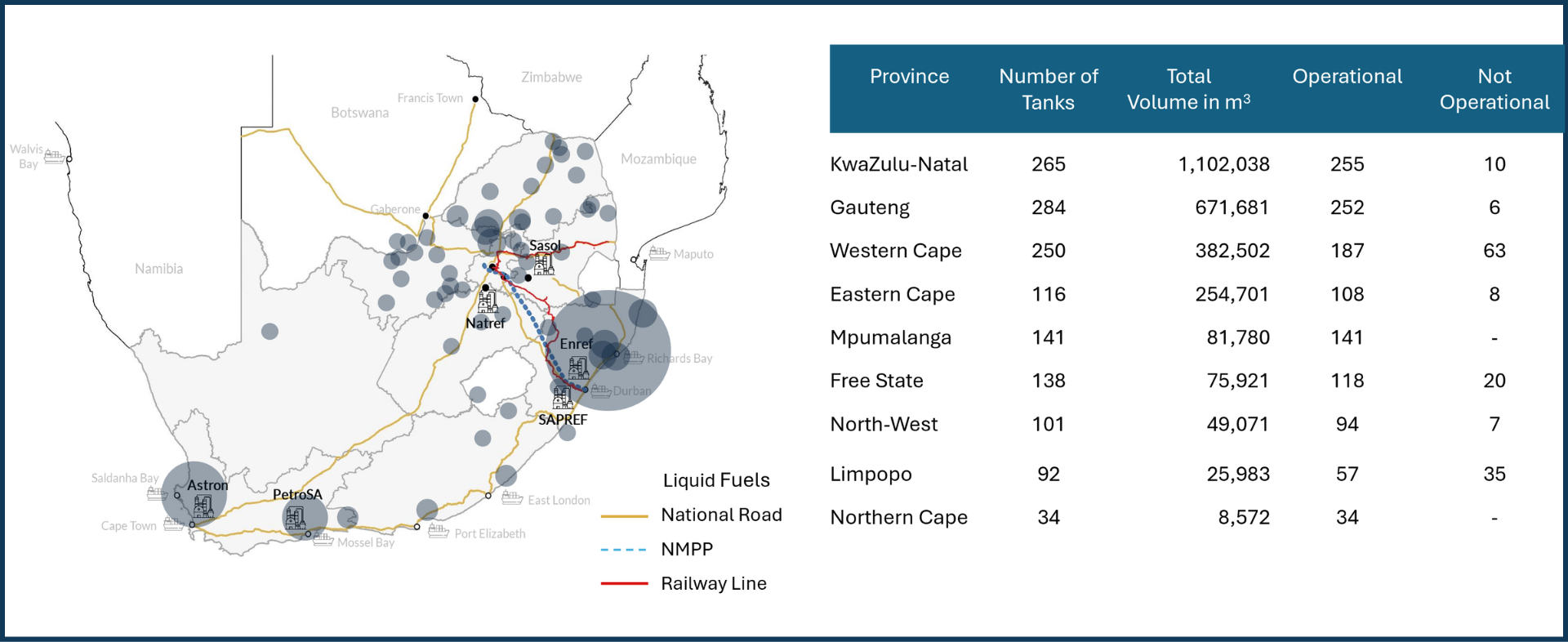

As refining declines, imports concentrate through specific coastal nodes. Durban remains the primary import hub for refined product. Its storage capacity, berthing infrastructure and pipeline connectivity make it central to inland supply. A significant share of diesel and petrol imports enter through this corridor before moving inland via pipeline toward Gauteng , as shown in Figure 2.

Cape Town handles imports primarily serving the Western Cape and aviation demand. Mossel Bay provides additional capacity but is more constrained relative to Durban.

If Durban experiences congestion, weather disruption, labour action, or infrastructure failure, the impact cascades inland. Gauteng, the country’s primary economic engine, depends heavily on product flowing from coastal terminals. In an import-led model, resilience depends not only on aggregate storage capacity but on geographic distribution of that capacity relative to demand centres.

Storage ratios reinforce the importance of this corridor. Coastal tankage around Durban holds substantially larger inventories relative to local demand because it functions as the country’s primary import reception and redistribution node. Inland demand centres, despite accounting for a large share of national fuel consumption, rely heavily on this coastal storage and the pipeline infrastructure that moves product inland.

Understanding storage reliance requires understanding demand geography. The largest concentration of fuel demand sits inland, particularly in Gauteng, which accounts for a substantial share of national petrol and diesel consumption. Industrial activity, freight movement, and urban mobility drive demand away from the coast.

Diesel demand is particularly sensitive. Mining, logistics, agriculture and backup generation all depend heavily on diesel availability. Any disruption in coastal import absorption can translate into inland supply stress rapidly.

Jet fuel demand concentrates around major airports. OR Tambo and Cape Town International are both reliant on consistent import and storage throughput. For example, OR Tambo’s supply chain is structurally concentrated. Most of its jet fuel has historically been supplied by Natref and transported inland through the pipeline network. Alternative supply depends on coastal imports, storage at port terminals, and redistribution inland via pipeline or road.

If Natref experiences operational disruption, maintenance delays, or throughput reductions, as occurred in 2025, OR Tambo’s primary supply channel tightens immediately. The system must then rely more heavily on imported product moving from coastal terminals through storage facilities and pipeline corridors.

In a stable environment, that transition is manageable. In a constrained environment, whether due to port congestion, shipping delays, pipeline maintenance or geopolitical disruption, the margin can narrow quickly. Because Jet fuel is not easily substituted in the short term. Aircraft operations depend on consistent supply and controlled storage conditions. Inventory buffers at airports are finite. Delays in replenishment can cascade into flight scheduling disruption, cargo delays, and broader economic impact.

In this configuration, storage at coastal nodes is not simply about local supply but about sustaining inland economic world’s medium-sour crude supply originates from the Gulf, including Omanvity.

Geopolitical Exposure and External Shock Transmission

Import dependency also increases exposure to geopolitical instability. A significant portion of refined product trade routes intersect with regions experiencing heightened geopolitical tension, particularly around the Middle East and adjacent shipping corridors. Disruptions in these regions affect freight rates, insurance costs, shipping times and cargo availability. Even absent direct supply interruption, volatility transmits through pricing and scheduling.

In a refinery-led system, crude supply volatility affected input cost but not necessarily physical availability of product. In an import-led system, refined product availability itself becomes exposed to global shipping dynamics.

If a shipment is delayed, and tank capacity is limited, the domestic buffer erodes quickly. Geopolitical risk from a South African context becomes a looming reality in ensuring security of supply of refined product.

Oman Case Study: Oil Soars Above $150 per Barrel

A recent example from global markets illustrates the constraints within refining systems. A large share of the world’s medium-sour crude supply originates from the Gulf, including Oman, which serves as a key benchmark and export stream for Asian refiners. This concentration means that disruptions, pricing shifts or logistical constraints affecting Gulf supply can have system-wide implications.

However, the availability of crude in the market does not imply that it can be readily used by any refinery. Refining systems are designed around specific crude slates, with configurations calibrated to density and sulphur characteristics. Even where a broadly comparable grade is available, substitution is not straightforward.

Switching crude inputs can alter product yields, affect unit performance and introduce operational risk. For example, changes in sulphur content or crude composition can impact downstream processing units, product specifications and refining margins. As a result, operators often avoid switching feedstock unless the implications are well understood.

These constraints are more pronounced in older or less complex refineries, where processing flexibility is limited. Facilities in parts of Asia, including Japan and Southeast Asia, may be technically capable of running alternative grades but are operationally cautious due to uncertainty around output and efficiency.

Substitution is therefore not only a question of availability, but of compatibility and confidence. The presence of alternative crude supply does not guarantee immediate adjustment within the refining system.

The implication is that upstream flexibility is structurally constrained. When disruptions affect key supply streams such as Gulf medium-sour crude, the system cannot always rebalance quickly through refinery substitution. In such conditions, downstream buffers particularly storage and inventory become critical in maintaining continuity of supply while adjustments work through the system.

Storage Capacity as the Core Resilience Variable

In this structural configuration, storage defines stability. Tank capacity determines how many days of supply can be maintained if cargo arrivals are delayed. Throughput capacity determines how quickly shipments can be discharged and moved inland. Geographic distribution determines whether supply shocks remain localised or propagate across the system.

Regional storage data highlights how this buffering function operates. Coastal import nodes such as Durban hold inventories that appear large relative to local consumption because they absorb cargo arrivals and supply inland markets as shown in Figure 3. Inland regions, where demand is highest, operate with materially smaller storage buffers relative to consumption.

High days-of-cover values at coastal nodes reflect logistics throughput rather than isolated regional supply security. Tanks at these import nodes absorb cargo cycles and sustain inland supply, particularly toward Gauteng. If storage capacity is insufficient relative to import volumes and demand concentration, the system operates with minimal elasticity. External volatility translates quickly into domestic constraint.

The gasoline storage ratios provide an additional illustration of how infrastructure interacts with demand measurements. In Figure 3, inland gasoline shows unusually high days-of-cover because storage at distribution depots is measured against a relatively small demand base in the calculation. In practice these facilities support wider regional distribution networks and logistics flows, meaning the storage serves a broader supply system than the local demand figure alone suggests. It also reflects demand dynamics: gasoline demand is expected to grow more slowly than diesel, leaving existing storage capacity relatively large relative to projected consumption.

| Fuel Type | Regions | Storage (Litres) | Estimated Days of Supply Cover |

|---|---|---|---|

| Diesel | Western Cape and Northern Cape | 156,324,800 | 23.58 |

| Eastern Cape | 124,561,000 | 34.01 | |

| Kwazulu Natal | 670,763,200 | 71.13 | |

| Inland - MP/GP/LP/FS/NW | 429,969,445 | 19.21 | |

| Gasoline | Western Cape and Northern Cape | 125,503,500 | Demand Fully Covered by Local Supply |

| Eastern Cape | 76,147,000 | 41.10 | |

| Kwazulu Natal | 342,905,700 | 87.79 | |

| Inland - MP/GP/LP/FS/NW | 359,560,860 | 900.22 | |

| Jet Fuel | Western Cape and Northern Cape | 29,432,740 | Demand Fully Covered by Local Supply |

| Eastern Cape | 18,261,000 | 13.84 | |

| Kwazulu Natal | 69,557,000 | 229.92 | |

| Inland - MP/GP/LP/FS/NW | 60,454,000 | 37.41 |

Figure 3: Estimated Days of Supply Cover (DMRE - SA Fuel Sales Volume data, NERSA Data,2025)

Why this Matters and What Next?

If storage capacity is adequate, diversified and aligned with inland demand corridors, the system gains resilience. In an import-led fuel economy, tanks increasingly replace refineries as the primary shock absorbers of supply volatility.

Energy security can therefore no longer be framed solely in terms of refining capacity. It should be assessed against refined product import dependency, days-of-cover relative to demand, the balance between strategic and commercial stockholding, port diversification, and the geographic distribution of storage relative to inland consumption.

The question is no longer whether South Africa should refine more. It is whether the liquid fuels value chain has sufficient storage elasticity to absorb disruptions in global shipping and maintain inland supply without cascading economic consequences.

In an import-led system, storage adequacy is not only an operational issue but also a financial one. When supply chains operate with thin buffers, volatility increases, and volatility is priced. Lenders, insurers and counterparties incorporate that risk into financing structures and operating costs. Over time, insufficient storage capacity does not only increase the probability of disruption; it raises the cost of doing business across the economy.

In this sense, storage infrastructure is no longer a peripheral asset in the fuel value chain. In an import-led fuel system, it becomes a strategic layer of national economic resilience, determining whether global supply disruptions remain logistical challenges or escalate into broader economic shocks

Mar 2026 Oil & Gas Policy & Regulatory Affairs Transport Infrastructure Supply Chain & Distribution African Competitiveness Energy Transition