Africa’s infrastructure deficit is well understood. Annual investment sits at roughly 3% of GDP, against an estimated requirement of at least 5.6%, while the African Development Bank places the financing gap at over $100 billion a year. Those numbers explain the scale of the problem, but they do not explain why some projects move while others remain trapped in pipeline.

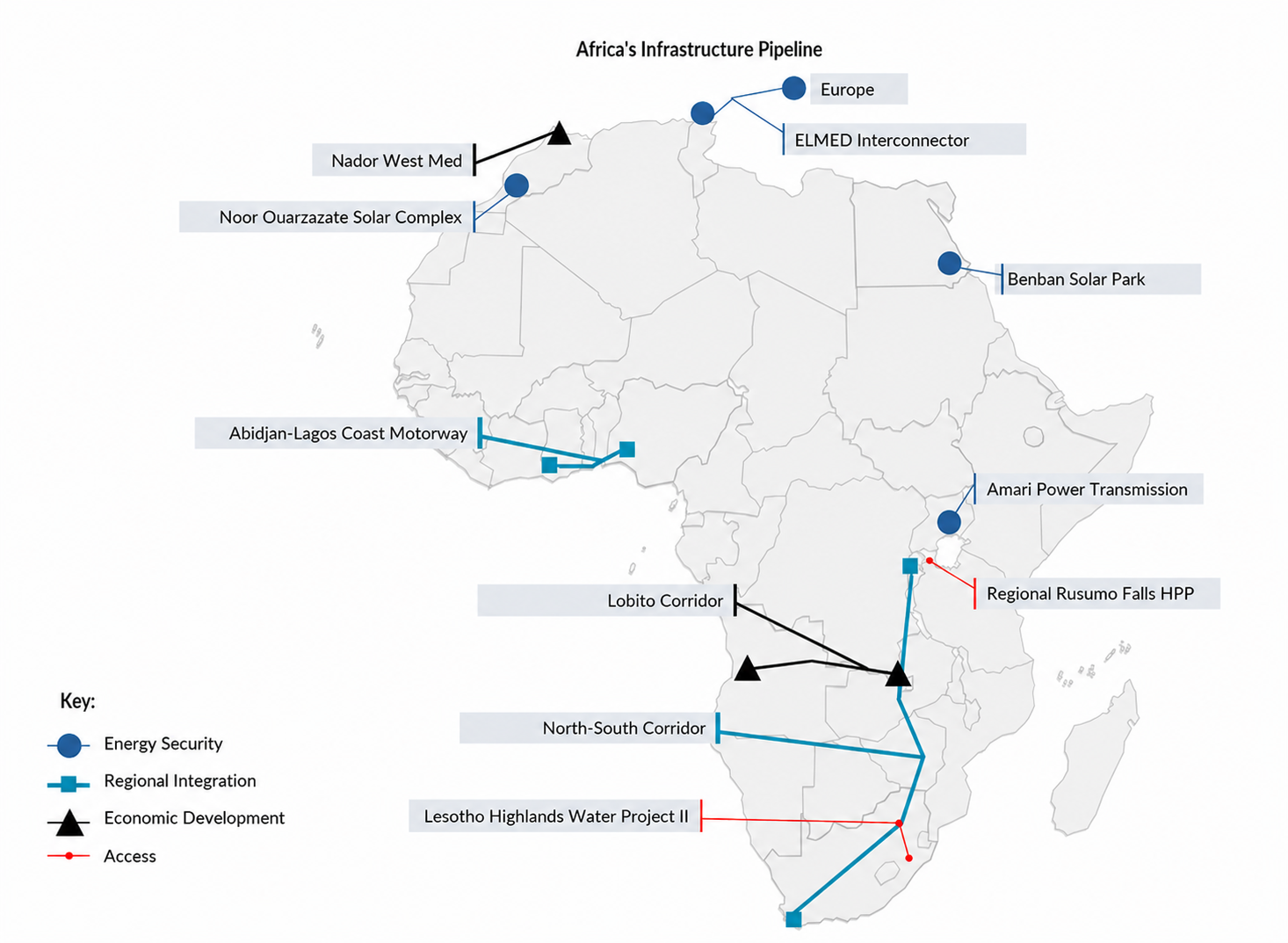

That distinction matters as the DEVAC Infrastructure Summit 2026 convenes. Across the continent, a select group of projects is progressing through financial close, construction, or operation. They sit across different sectors: regional integration, access, economic development, and energy security, but they raise the same underlying question: what conditions allow infrastructure to survive the long path from announcement to delivery?

This article examines that question through a selection of flagship projects across the continent. The focus is not only on what these projects are built to unlock, but on the institutional, regulatory, commercial, and execution conditions that allow them to move.

A pipeline shaped by institutional conditions

The OECD’s Africa’s Development Dynamics report states that raising annual infrastructure investment to $155 billion could lift GDP growth by 4.5% and, potentially, double the continent’s GDP by 2040. Inadequate infrastructure reduces business productivity in Sub-Saharan Africa by up to 40%, and erratic electricity supply in South Africa alone is estimated to have reduced that country’s GDP by 2% during peak power disruptions. The projects examined span four outcome categories: regional integration, access, economic development and energy security.

Infrastructure begins to scale when coordination exists above the sovereign level

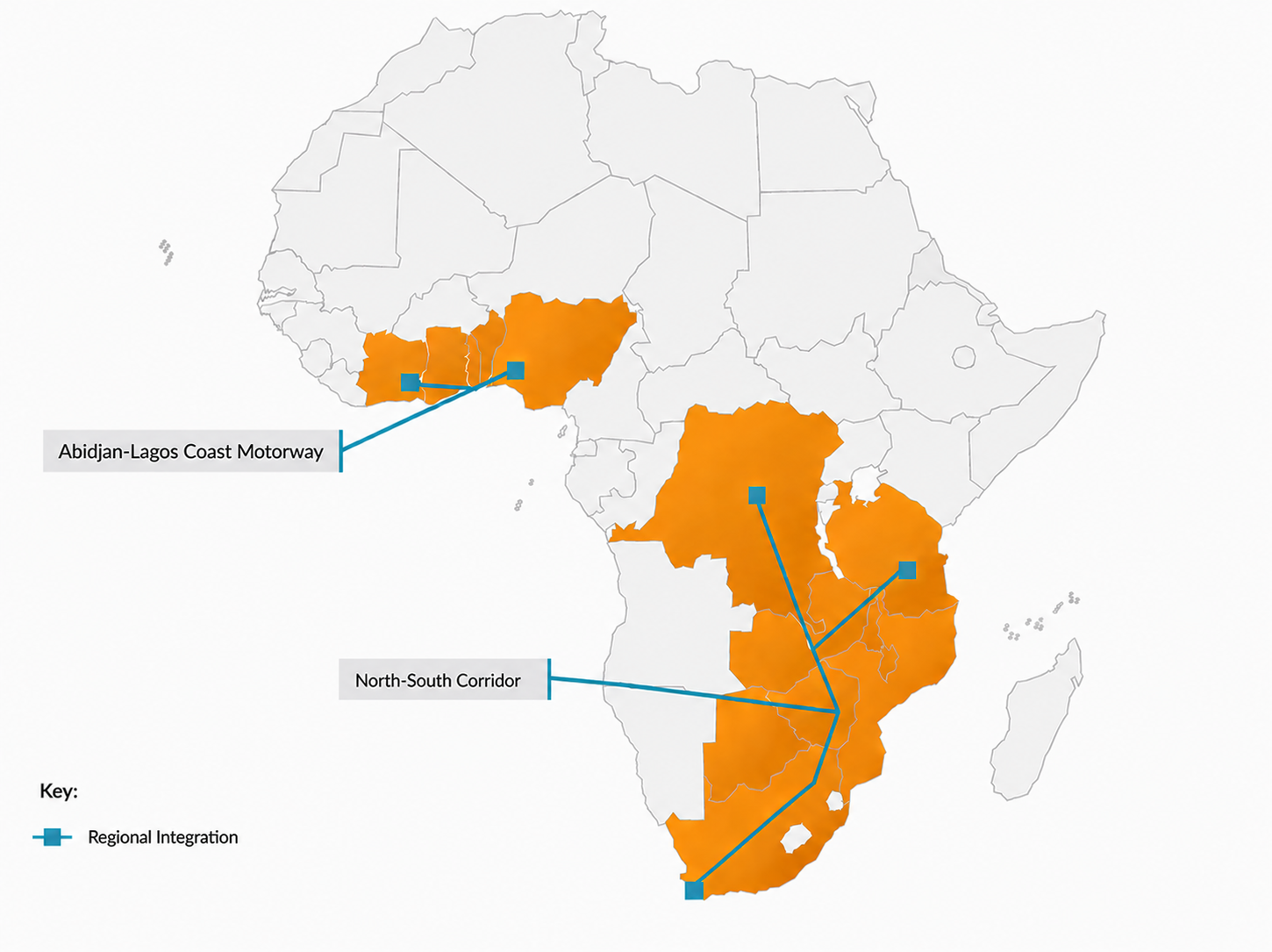

Intra-African trade reached $192.2 billion in 2023, representing 14.9% of the continent’s total trade, according to Afreximbank. The United Nations Economic Commission for Africa (UNECA) projects a 35% increase upon full implementation of the African Continental Free Trade Area. The caveat is that the relationship between trade liberalisation and value chain formation is dependent on logistics and regulatory capacity. Physical connectivity between countries is a precondition for any of those projections to materialise.

The Abidjan–Lagos Coastal Motorway, extending approximately 1,028 km across five West African countries, advances under ECOWAS, which holds a harmonisation mandate that individual member states cannot exercise independently. In Southern Africa, the North-South Corridor, an established trade artery that carries approximately 60% of SADC trade across seven member states and directly serves half the region’s population, is undergoing a transformation. SADC’s July 2025 endorsement of an economic corridor pilot programme estimates it may unlock $16.1 billion in regional GDP and 1.6 million jobs. Although both corridors fall under the African Union’s Programme for Infrastructure Development in Africa at the continental level, their operational frameworks differ: ECOWAS governs the Abidjan-Lagos corridor, and SADC governs the North-South upgrade.

Access infrastructure depends on institutional durability more than engineering complexity

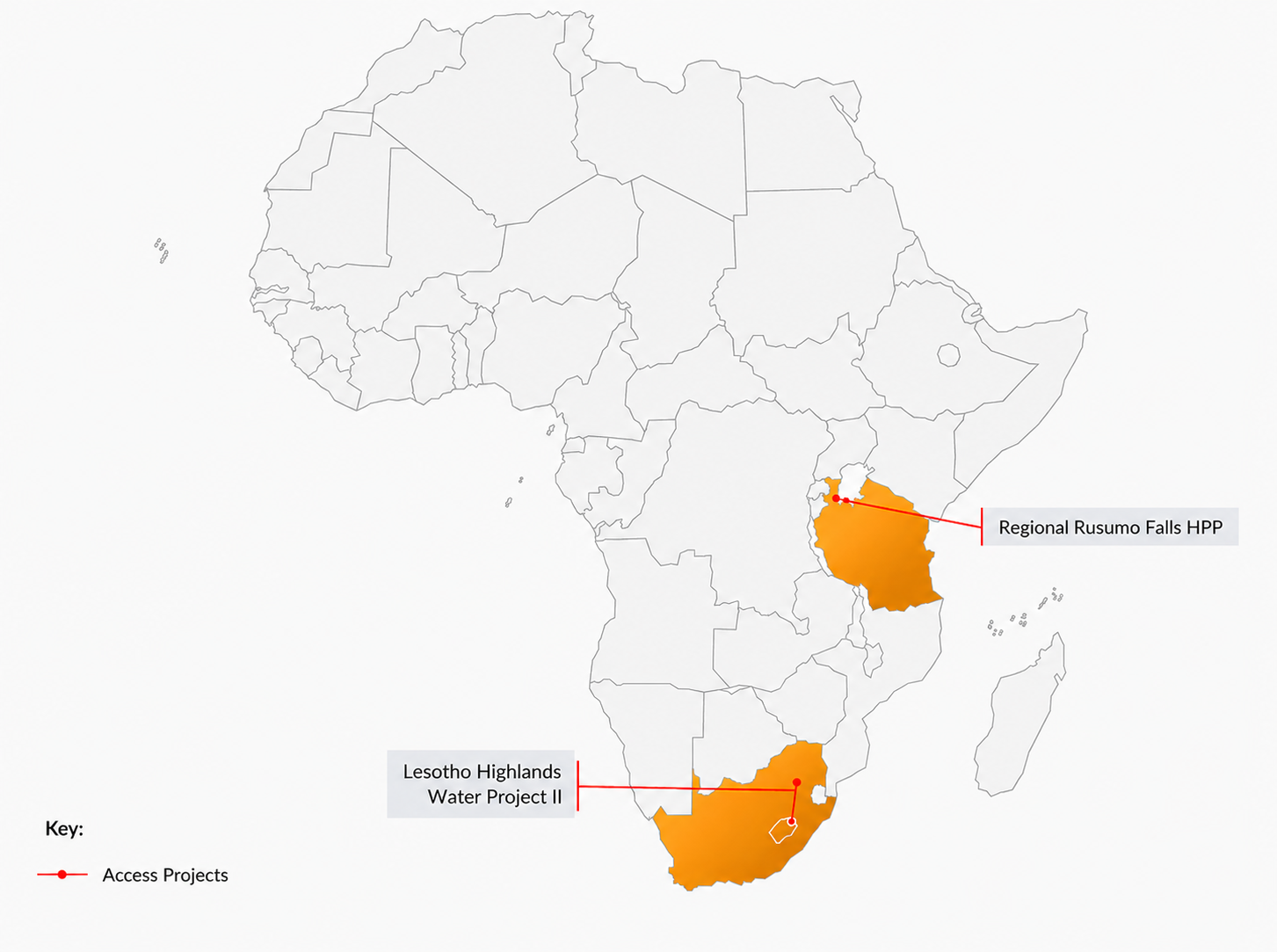

The Regional Rusumo Falls Hydroelectric Project supplies 80MW jointly to Burundi, Rwanda and Tanzania from a tri-national Special Purpose Vehicle (SPV) established by the respective governments. The project has an estimated cost of $468.6 million and is financed by the World Bank and the AfDB. Since commissioning in 2023, the plant has delivered 66 million kilowatt-hours in its first three months, with projected benefits for approximately 1.1 million people across the three countries, improving electricity access from 4% for Burundians, 13% for Rwandans, and 15% for Tanzanians in 2013, at the time of project approval. Institutional design, in the form of equal ownership, equal allocation, and binding intergovernmental agreements codified before construction, played a key role in facilitating the project.

The Lesotho Highlands Water Project Phase II, comprising the Polihali Dam and a 38-kilometre transfer tunnel delivering water from Lesotho’s highlands to South Africa’s Gauteng province, with royalty payments flowing back to Lesotho in exchange, illustrates how a bilateral treaty signed in 1986 between Lesotho and South Africa has enabled successive delivery cycles across multiple political transitions.

The pattern is consistent but must be qualified. The Kikagati-Murongo Hydropower Plant on the Kagera River, a $100 million bilateral project between Uganda and Tanzania, stalled from its inception in 2005 until a binding bilateral agreement on power sharing was reached in 2017, after which the project proceeded to commissioning in 2023. The project’s long dormancy advances the argument for the enabling role of institutional arrangements. The Ruzizi III Regional Hydropower Project, a 206 MW Scheme across Rwanda, Burundi, and the Democratic Republic of the Congo (DRC), structured under the CEPGL framework, with a tripartite agreement signed in 2019 and an estimated cost of $644-700 million, demonstrates the converse. Formal institutional structure is a necessary condition, but that alone is not sufficient. Political instability in the DRC and financing complexities extended the pre-construction period to more than six years, with construction only commencing in late 2025.

Where institutional arrangements are formally documented, jointly governed and durable across political cycles, the probability of delivery increases measurably, but other variables - including political economy and capital structure – remain operative.

Capital becomes more efficient when infrastructure sits inside a value chain

Where infrastructure anchors an industrial value chain, it can attract long-tenor commercial capital on terms that development finance alone cannot replicate. The Lobito Corridor, connecting Angola, the DRC and Zambia, is structured around documented offtake agreements across all three jurisdictions, a mineral corridor of particular relevance to the global energy transition. The DRC holds approximately 71% of global cobalt reserves and accounted for 80% of global cobalt output in 2024.

Zambia, on the other hand, accounts for roughly 4% of global copper output, making it the continent’s second-largest copper producer. The documented architecture attracted a $753 million financing package closed in late 2025, comprising a $553 million United States Development Finance Corporation loan and $200 million from the Development Bank of Southern Africa. Capital of tenor reflected that not only engineering quality but commercial structure, geopolitical relevance, and Development Finance Institution mandates may have also been operative factors, but without the documented value chain logic, comparable terms would not have been available.

Energy security infrastructure moves faster because the cost of delay is higher

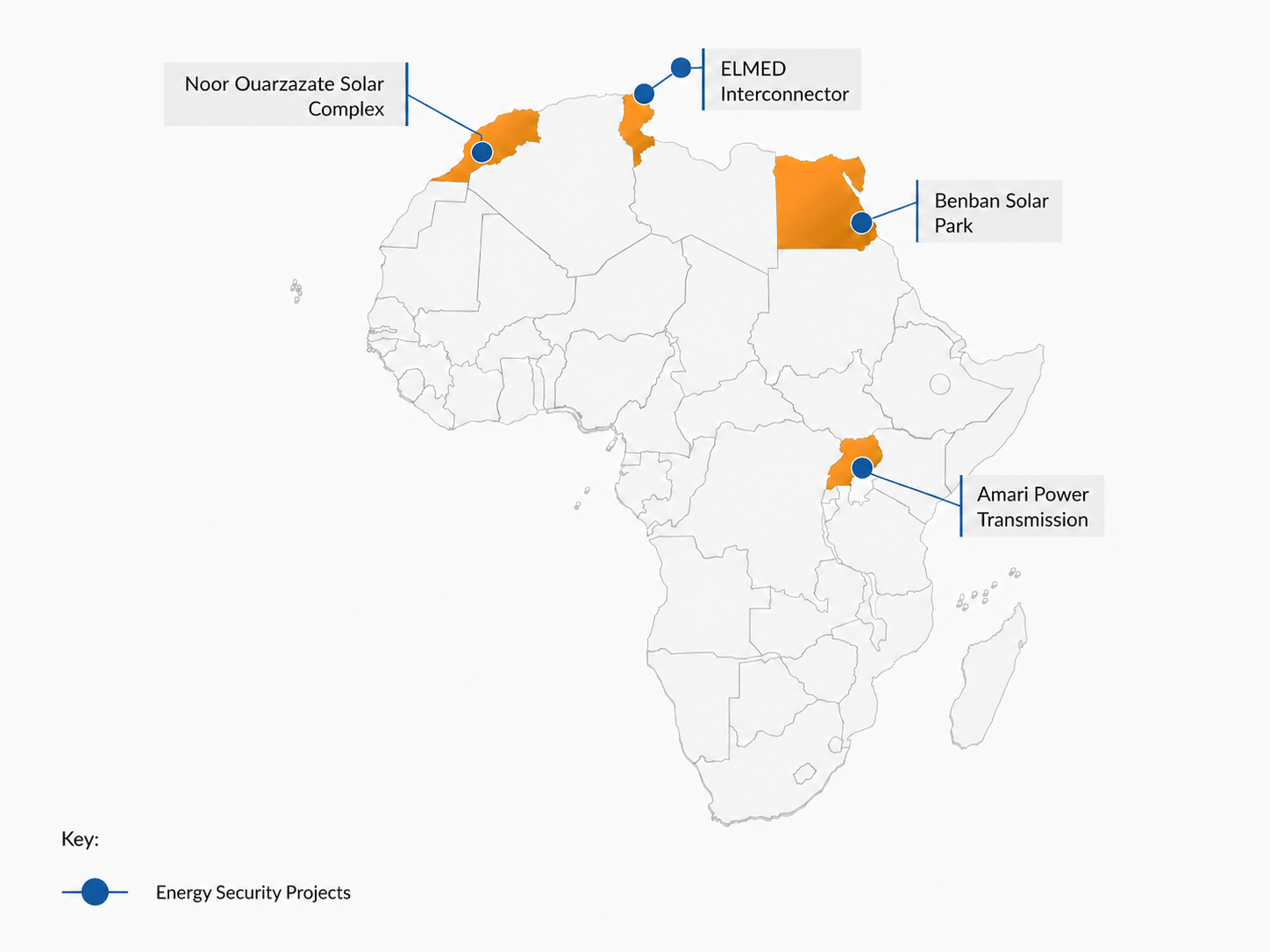

A further category covers infrastructure built to harden energy and supply systems against climate and geopolitical shocks. The ELMED interconnector, a 200-kilometre, 600-MW high-voltage direct current submarine cable at an estimated cost of approximately $1.2 billion, anchored by a $336 million EU Connecting Europe Facility grant, reduces Tunisia’s longstanding dependence on Algerian imports, which account for 15% to 20% of peak demand, while repositioning North Africa as a credible supply node for European energy security. The Amari Power Transmission Project, a USD 50 million independent transmission project in Uganda that reached financial close in March 2026, proves that private capital can work in African power transmission, not just generation.

Morocco's Noor Ouarzazate (510 MW and over $9 billion in total programme investment) and Egypt's Benban Solar Park (1.8 GW and $4 billion programme investment) address fossil fuel import dependence through different institutional instruments. Morocco reduced its energy import dependence from over 97% in 2009 to approximately 86% by 2023, whereas Egypt’s renewable capacity expanded from under 4 GW in 2015 to over 10 GW by 2024. Noor Ouarzazate is operated by MASEN, Morocco's dedicated renewable energy agency. Benban operates on standardised 25-year power purchase agreements backed by International Finance Corporation (IFC) guarantees, with IFC leading a $653 million financing consortium and the Multilateral Investment Guarantee Agency providing $210 million in political risk insurance. Neither uses standard ministerial procurement because, at this scale, it results in longer cycles and weaker investor confidence.

The projects reveal the same pattern

These projects do not suggest that infrastructure delivery constraints across the continent have been resolved. Large portions of Africa’s pipeline remain delayed between feasibility, procurement, financing, and execution. What these projects demonstrate, however, is that the institutional conditions required for delivery are increasingly visible and, in several cases, repeatable.

Across sectors and geographies, the same underlying pattern emerges. Regulatory clarity improves the ability of capital to price risk. Coordinated institutions sustain delivery across political and financing cycles. Commercial structures linked to identifiable demand improve financing efficiency. Delivery capacity determines whether projects survive the years between announcement and operation.

The implication is that infrastructure outcomes are becoming less dependent on project ambition alone and more dependent on the systems supporting execution. As infrastructure programmes increase in scale, complexity, and sovereign coordination, delivery architecture increasingly determines whether projects progress or remain suspended within pipeline.

The continent’s infrastructure challenge is therefore becoming more institutional than conceptual. The projects already in motion provide evidence of what delivery requires in practice. The question now is whether those conditions can be replicated consistently enough for infrastructure execution to scale beyond a limited set of flagship programmes.

02 June 2026 Policy & Regulatory Affairs Bilateral & Multilateral Partnerships Transport Infrastructure Trade & Facilitation Public Service Transformation Financing Growth & Development in Africa

Kayla Govender-Seetal

Mthabisi Khumalo